Note: If you're viewing on the support chat widget, we recommend you click the expand icon ![]() on the top right corner, for better viewing experience.

on the top right corner, for better viewing experience.

Introduction

The Aged Receivables report is an essential tool in keeping track of all your outstanding payments. This report is primarily used by the person-in-charge of collections but is also helpful when writing off bad debts.

Failure to collect outstanding payments in a timely manner more often than not results in a disruption of your business's cash flow. Such a scenario is highly unfavourable and thus the importance of an Aged Receivables report to better help business owners better manage it.

What's in an Aged Receivables Report?

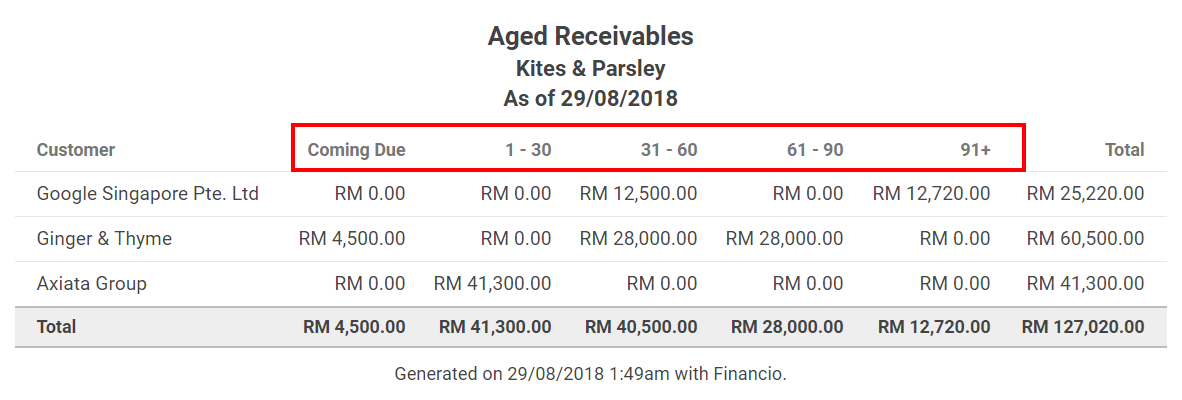

The first thing you'll notice in the first column of your Aged Receivables report is the customer list. From here, you'll be able to easily track all your customers with outstanding payments due.

In the row across, you'll find the duration/period. Coming due shows the outstanding amount that is still within the agreed payment terms. Once payment becomes overdue, the Aged Receivables report will start tracking based on a "30 days category".

What do I do with this information?

- Evaluating Credit Terms - Managing your cash flow from an early stage is vital to the success of your business. If you are struggling with large amounts of overdue payment, perhaps limiting the credit extended to each customer will help you better manage it.

Requesting for a deposit or a 50% upfront payment are amongst the many ways of mitigating this risk. - Accounting for Bad Debt - Unfortunately, at some point, an invoice that is not paid up has to be written off your books and be recorded as a Bad Debt. It is up to the business owner to determine when an invoice is deemed as uncollectible and for it to be written off as a Bad Debt. Some may have it written off after the 90 days overdue period while others may extend as far as an entire year.

There are 2 ways to account for Bad Debts:

- Direct Write-Off Method: Using this method, you'll simply issue a credit note on the issued invoice and charge the amount under a Bad Debt Expense account which you'll need to create in your chart of accounts. This, however, is not the preferred method as it only recognizes the Total Bad Debt Expense once it becomes uncollectible.

- Bad Debt Allowance Method: With this method, you'll be able to estimate and recognize the Total Bad Debt Expense before they are deemed uncollectible. This will allow time for business owners to make the necessary changes to mitigate further bleeding.

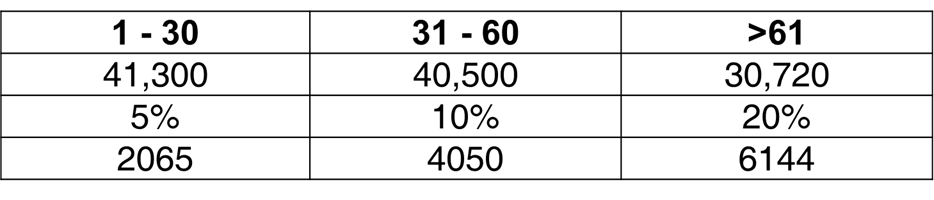

To implement this method, you'll first have to determine the percentage of overdue payments that typically becomes uncollectible. This can be done using historical experiences with bad debt.

For example: 5% bad debt on overdue payment in the 30 days category, 10% bad debts in the 31-60 days category and 20% bad debts in the > 61 days category.

Referring to the earlier Aged Receivables Report, you'll be able to quickly work out the total Allowance for Doubtful Accounts for this period.

In this example, the total Allowance for Doubtful Accounts:

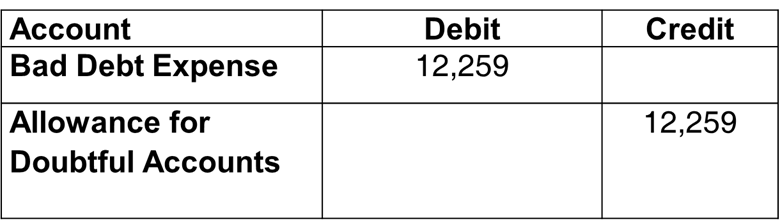

From here, simply create an Allowance for Doubtful Accounts under your Current Assets and a Bad Debt Expense category under expenses in your chart of accounts. Next, create a Journal Entry as follow:

The Bad Debt Expense will serve as a controlled account to ensure while the Allowance for Doubtful Accounts will reflect the reduction in your Accounts Receivable and show a more accurate representation of your total assets.

- Writing-Off a Bad Debt: To do this, go ahead and issue a credit note on the related invoice as per the normal process. Instead of charging it to the Bad Debt Expense, this time you'll charge the Allowance for Doubtful Accounts instead to knock off the initial records.

And there you have it, a quick guide on how the Aged Receivables Report can be helpful in managing your business's cash flow and operations.

Comments

0 comments

Please sign in to leave a comment.