Note: If you're viewing on the support chat widget, we recommend you click the expand icon ![]() on the top right corner, for a better viewing experience.

on the top right corner, for a better viewing experience.

Profit & Loss report may also be referred to as:

- P&L

- Income statement

- Earnings statement

- Revenue statement

- Operating statement

- Statement of operations

- Statement of financial performance.

The Profit & Loss report is undoubtedly one of the most important reports for business owners. Here are 3 key functions of the report:

- Required filing by Singapore and Malaysia authorities - While this only applies to companies that meet the requirements by ACRA and SSM respectively, it is generally a good idea to start early.

- Applying for small business loans - With a proper Profit & Loss report, a small business will find it much easier to get their loans approved.

- Business decision-making processes - With a clear understanding of a business's net income, a business owner will be able to make better decisions and put the business on the right track for growth.

So what exactly is a Profit & Loss report?

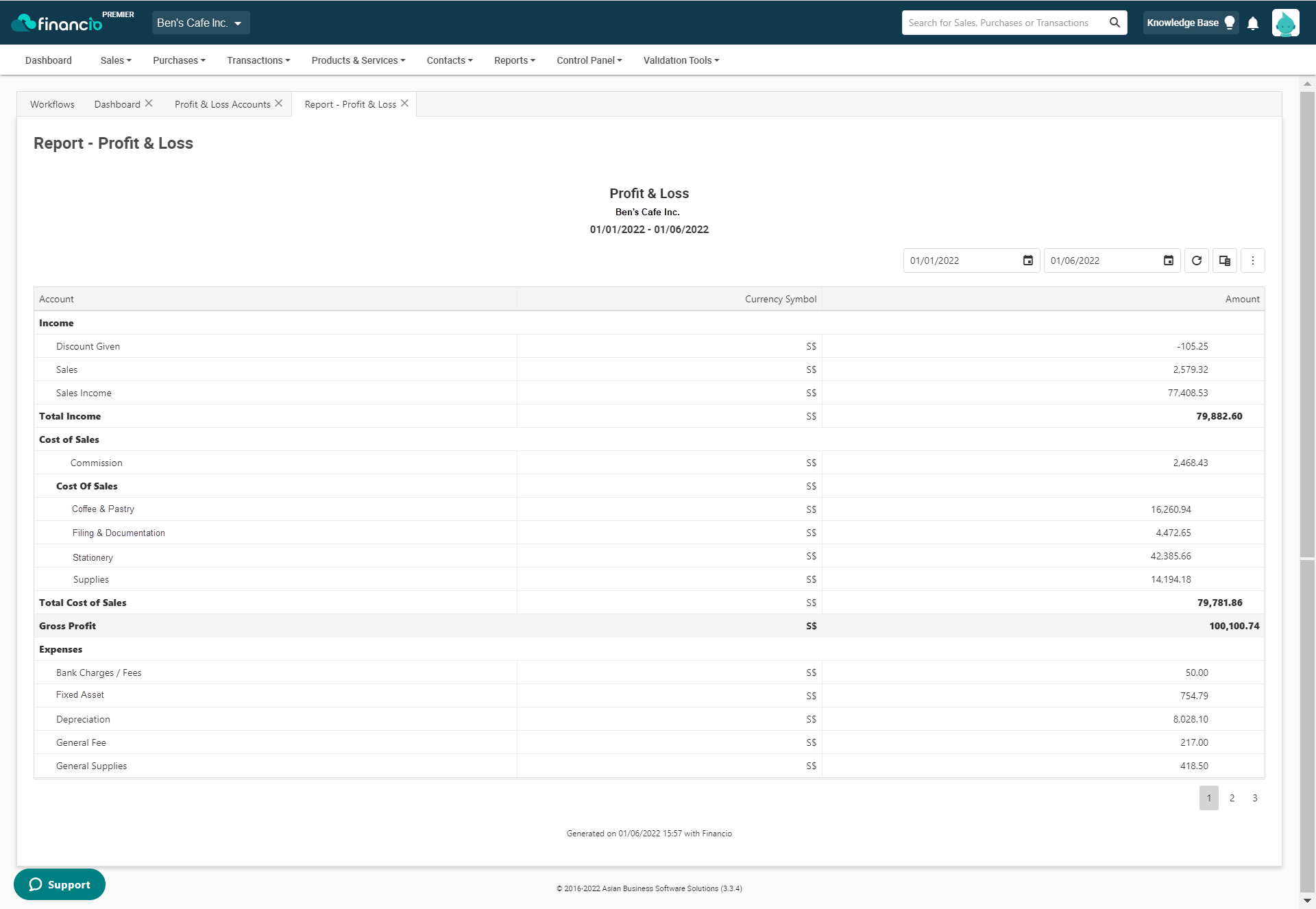

It is basically a 3-part document that shows a business' Total Income (Revenue), Total Cost of Sales and Total Expenses. By deducting the Total Cost of Sales and Total Expenses from the Total Income (Revenue), a business is able to determine the net earnings/net income of a given period.

Total Income less Total Cost of Sales = Gross Profit/Gross Income

Gross Profit less Total Expenses = Net Earnings/Net Income

How is this bit of information helpful? - Occasionally, a business may report high revenue but negative net earnings/net income in a given period due to higher expenses. With the help of the report and some financial formulas - Operating Expense Ratio (OER) / Profit Margin Ratio, a business owner will have a better understanding of a business' effectiveness in generating income.

How to create a Profit & Loss report?

Despite being one of the more complicated reports to prepare, with a little accounting knowledge and some practice, anyone can produce the report as long as all items under the income, cost of sales and expenses have been recorded correctly.

Comments

0 comments

Please sign in to leave a comment.